The road to $20trn: how ETFs reshaped crypto in recent years

How ETFs hit $20trn, bridged TradFi and crypto, and what comes next.

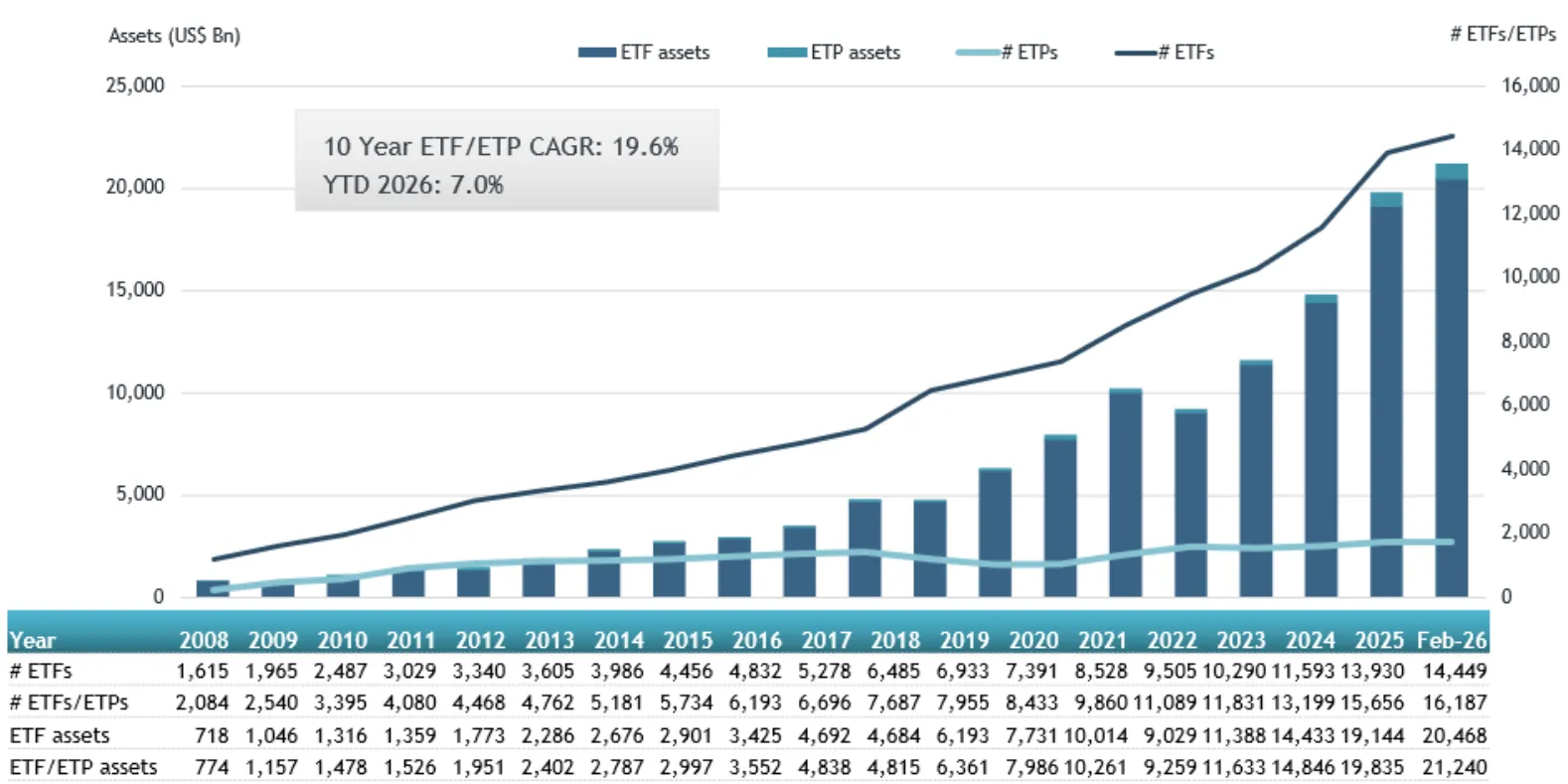

Exchange-traded funds (ETFs) have travelled from experiment to staple of modern finance. In 2026, assets under management (AUM) in ETFs topped $20trn.

How these vehicles rewired investing, opened a bridge to crypto, and why direct indexing is hailed as the next stage in portfolio evolution—explained by ForkLog.

How ETFs work

An ETF is a separate legal entity that holds a basket of assets which, depending on regulation, may include securities, commodities, derivatives and cryptocurrencies.

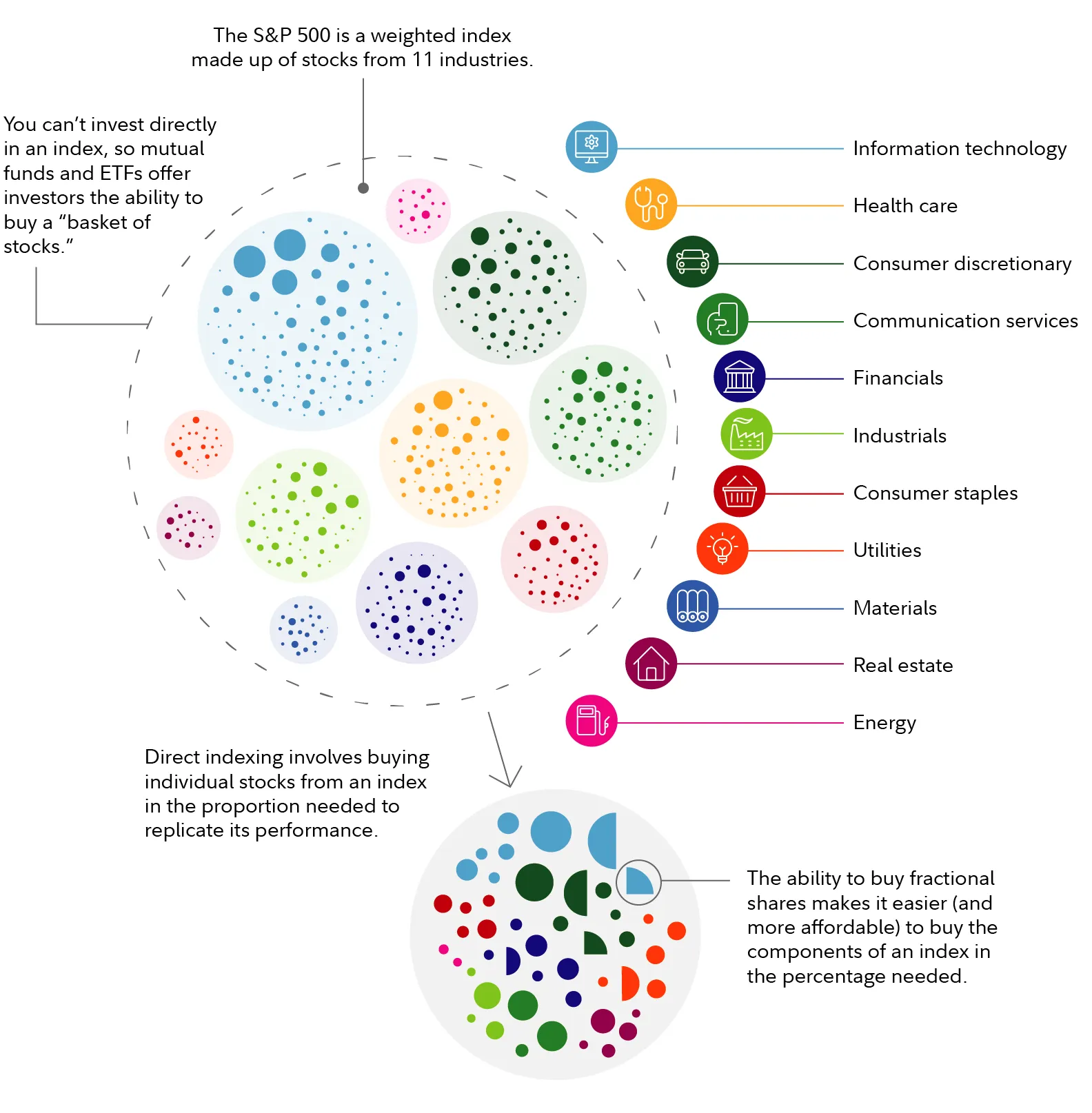

Each share is backed by a slice of the fund’s holdings: investors get exposure to a portfolio without owning the underlying assets directly. Buying all S&P 500 constituents piecemeal would require substantial capital and extra costs. An ETF simplifies this: the manager assembles a portfolio mirroring the index, then issues fund shares backed by those assets. With a single purchase, an investor gets a micro-stake in all 500 firms.

ETF prices usually sit close to net asset value thanks to an arbitrage mechanism run by large banks—authorised participants (APs). Retail investors do not take part.

If ETF shares trade above the value of the underlying, APs buy the underlying on the market, swap it with the fund for new ETF shares and sell them on exchange. The increased supply brings prices back in line (and vice versa).

Because little manual management is required, funds can keep fees razor-thin—down to a few basis points.

Before ETFs, pooled investing worked via mutual funds (the equivalent of PIFs), which had pricing drawbacks. Net asset value was calculated after the market close. Investors could buy or sell only once per day. Intra-day swings left them stuck without an exit. Markets needed a tool marrying the diversification and reliability of classic funds with the agility of equities.

In 1993 State Street Global Advisors launched SPDR S&P 500 (ticker SPY) in the US. Built to help institutions hedge swiftly, the passive SPY became a retail hit and set the gold standard for future ETFs thanks to transparency, low fees and intraday trading.

In the 2000s the industry moved beyond broad indices: BlackRock and State Street rolled out sector ETFs for targeted bets—from gold mining (SPDR Gold Trust) to innovative medicine. The concept later evolved into actively managed funds, where returns hinged on in-house trading teams.

For years the US Securities and Exchange Commission (SEC) resisted active ETFs. The sticking point was transparency: funds had to disclose their portfolios daily. Managers balked, fearing frontrunning and copycat strategies.

The first actively managed ETF was approved and launched in March 2008: Bear Stearns Current Yield (ticker YYY) from the eponymous bank. It hit the market days before the bank collapsed in the financial crisis and was hastily sold to JPMorgan Chase.

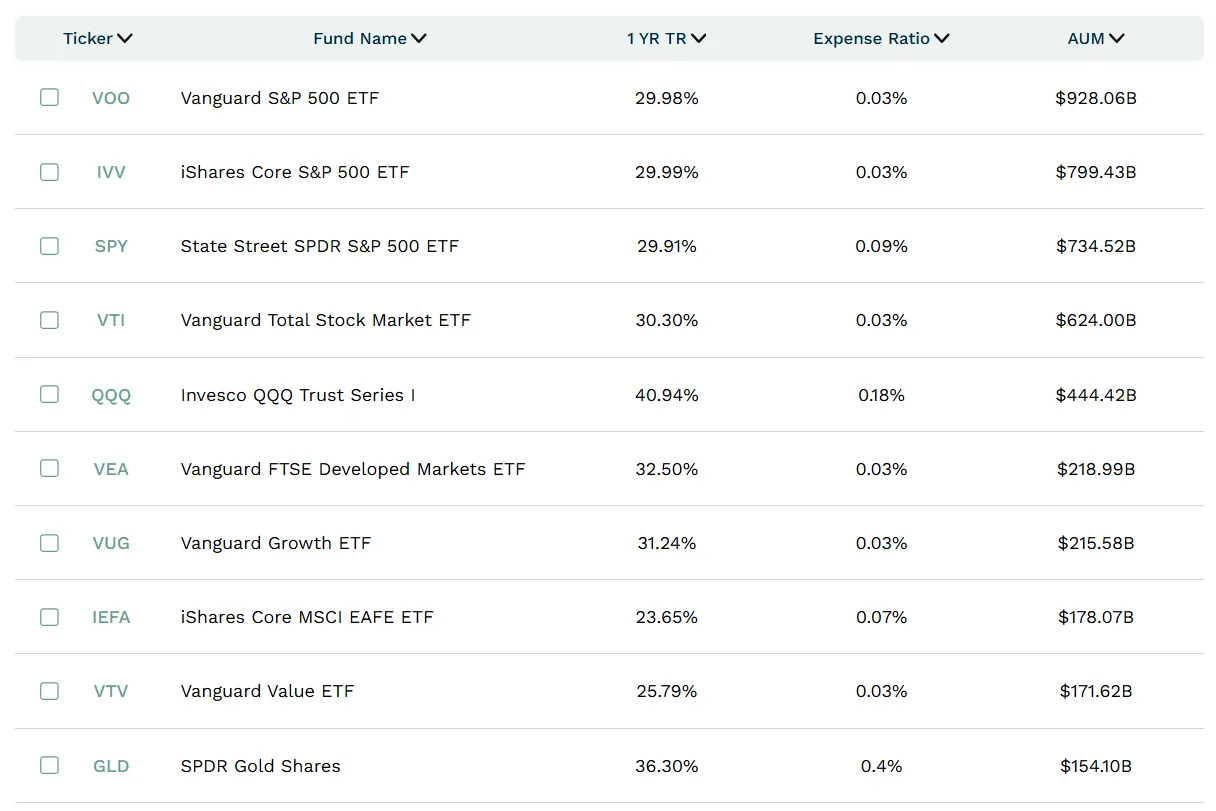

The crash dented confidence in active ETFs and turbocharged a shift to ultra-low-fee passive strategies, achieved by trimming “human” traders. Broad-market funds—VTI and VOO—went on to gather trillions.

To survive the fee war and stand out from giants like Vanguard, providers launched factor (smart-beta) hybrids. These pick constituents by rules—say, low volatility or value. It was a first step toward active management, but algorithmic.

In 2019 the SEC finally approved rules for such “semi-transparent” ETFs, letting managers package strategies without daily portfolio disclosure.

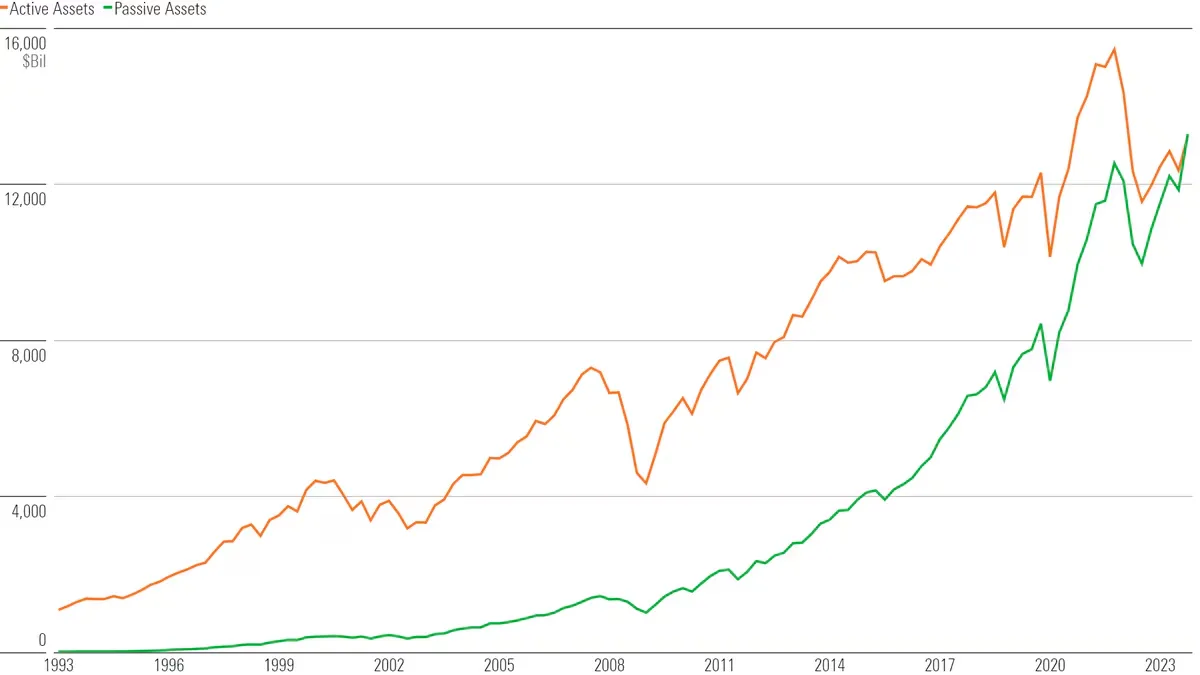

At the start of 2024, assets in passive funds in the US surpassed active for the first time. Investors recognised that, mathematically, it pays to track rather than pay up to try to beat the market. Even so, active ETFs still make up roughly 10% of ETF assets. In February 2026 they hit a new high of $2.15trn.

Beyond the Big Three

By February 2026, 14,449 ETFs were registered worldwide with AUM of $20.46trn, offered by 978 providers across 65 countries.

It is an oligopoly. Out of hundreds of providers, three financial behemoths control the lion’s share of assets:

- BlackRock (the iShares family) is the industry’s undisputed leader with AUM above $10trn. Its 2009 purchase of iShares from Barclays ranks among Wall Street’s most successful deals. Today BlackRock is a locomotive for integrating digital assets (RWA, crypto ETFs) into traditional finance.

- Vanguard, founded by indexing pioneer Jack Bogle, has a unique structure: it is owned by its own funds—its investors. It has long undercut rivals with ultra-low fees.

- State Street, a pioneer and creator of the S&P 500 fund, remains strong with institutional products and owns SPDR rights.

Asset concentration has made the “Big Three” among the largest shareholders in nearly all listed US companies, boosting their influence in proxy votes.

One outsider cracks the AUM top ten: Invesco QQQ Trust Series I. In 1999 Invesco bought PowerShares and with it the rights to manage the fund tracking the Nasdaq-100. It proved a gold mine. QQQ accounts for a sizeable share of the firm’s business.

In April 2026 BlackRock and State Street moved to erode Invesco’s position. They filed for their own Nasdaq-100 ETFs, seeking to end a long-standing monopoly on that index.

The industry has outgrown the narrow stereotype of “stock index trackers” and become a versatile wrapper for a host of financial ideas.

ETFs are commonly sorted by two axes: underlying asset class and strategy. The former includes equities, bonds, commodities and crypto.

The latter spans vehicles with varying complexity:

- thematic. Bets on long-term macro trends rather than classic sectors—for example AI, robotics, cybersecurity or clean energy;

- dividend or income. Portfolios are built to maximise investor cash flow;

- leveraged and inverse, for short-term aggressive trading. The former magnify index returns (eg 2x or 3x to the S&P 500). The latter rise when the index falls, enabling short exposure;

- options-based. The fund owns stocks and sells calls on them. Upside is capped, but current yield can exceed 10% annually;

- buffered. Capital-protected funds that seek to limit losses—say, to 10% in a sell-off—in exchange for a cap on gains (for example, no more than 12% in a year). Popular with conservative investors in times of uncertainty.

Wall Street wants blockchain

Crypto’s path to the stock market was long. For a decade the SEC rejected spot bitcoin ETF filings, citing weak surveillance and manipulation risks.

In 2023 the tide turned: a court victory by Grayscale over the SEC and a filing from BlackRock sped crypto’s integration into TradFi.

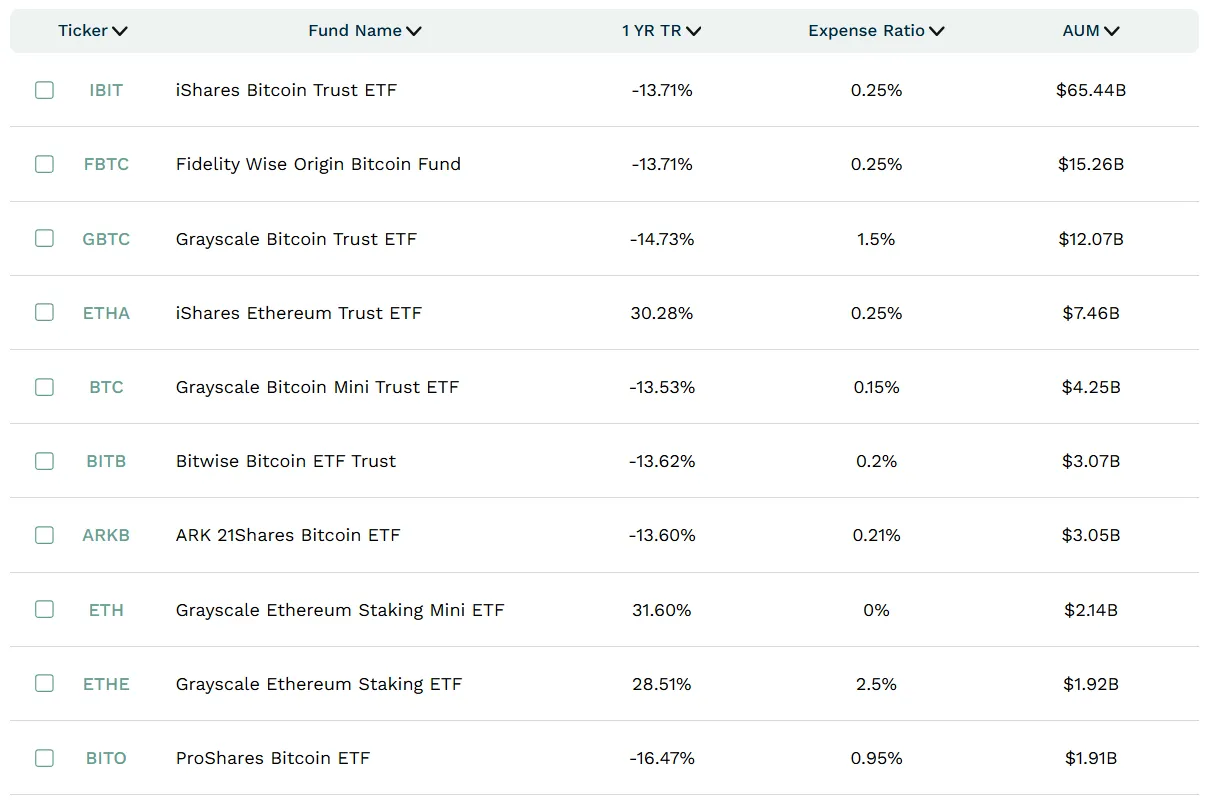

In January 2024 regulators approved the first 11 spot bitcoin ETFs, unleashing record inflows. Bitcoin was acknowledged as a macro asset at the institutional level.

That summer, the crypto-ETF line-up expanded to Ethereum-based funds. To preserve Ether’s status as a commodity within exchange products, providers agreed to exclude staking from fund structures. In October 2025 trading began in the first spot ETFs on Solana—a breakthrough that integrated staking rewards directly into the fund.

Unlike retail users who can buy tokens outright, crypto ETFs offer regulated access via familiar exchange instruments and solve several fundamental problems:

- infrastructure risk. Investors need not store seed phrases or build complex security stacks—licensed institutional custodians do it for them;

- regulatory barriers. Conservative institutions are often barred from buying crypto on spot venues, yet can purchase securities on Nasdaq or the NYSE;

- tax optimisation. In the US, buying ETFs via retirement and brokerage accounts can confer meaningful capital-gains benefits unavailable with direct token ownership.

In parallel with crypto ETFs, financial giants have moved into tokenisation of real-world assets. Whereas bitcoin serves as an ETF’s underlying, tokenisation brings traditional assets (bonds, gold, real estate) onto blockchains.

Franklin Templeton led the way in 2021 with Franklin OnChain U.S. Government Money Fund (FOBXX)—the first US fund to use Stellar and Polygon for transaction processing and ownership records. It invests in US Treasuries while recording share ownership on-chain. Investors can buy and move tokens 24/7.

In March 2026 the asset manager said it plans, with Ondo Finance, to issue tokenised versions of its ETFs, accessible directly via crypto wallets.

BlackRock has taken a similar step, launching BUIDL (BlackRock USD Institutional Digital Liquidity Fund) on Ethereum, giving institutions on-chain access to US Treasury yields.

On May 6th 2026, Morgan Stanley’s crypto push came into focus. The firm is preparing a tool to convert digital assets into ETF shares, alongside tokenised equities.

The backlash and direct indexing

Passive investing’s ascent has drawn heavyweight critics, among them Michael Burry of Scion Capital. Back in 2019 he called ETF inflows a negative force:

“The bubble in passive investing through ETFs and index funds, as well as the trend toward large-scale asset management, have left cheaper securities around the world orphaned.”

The rub is that index funds allocate capital by market capitalisation. In the S&P 500, that means heavy weightings to the largest tech firms—Apple, Microsoft and NVIDIA—because they dominate the index.

Burry argues this algorithmic approach distorts price discovery: market makers artificially inflate the capitalisations of monopolies, while starving promising small caps of liquidity.

The answer to these structural issues is direct indexing—the chief conceptual rival to ETFs. Instead of a single fund share, broker algorithms buy tiny slices of the index’s constituents directly into the client’s account. That avoids “blind” allocation: investors can fine-tune portfolios (manually excluding overpriced names) and optimise taxes through targeted loss harvesting.

Ideologically, direct indexing is close to crypto. Using non-custodial wallets, decentralised exchanges and programmable smart contracts for automated rebalancing lets Web3 users build their own “indices” without surrendering control or paying corporate fees.

Even so, for macro players and multi-billion-dollar funds, the simplicity, familiar plumbing and enormous liquidity of classic ETFs remain the overriding priority.

Over three decades, ETFs have evolved from technical experiment to financial bedrock. Crucially for Web3, they have become a lawful gateway for Wall Street liquidity to reach digital assets. Approvals for bitcoin, Ethereum and Solana funds show that conservative regulators can adapt to new technology.

Bringing Treasuries and corporate equities on-chain strips out intermediaries, delivering the 24/7 liquidity and transparency that early ETF architects only envisaged. Yet their spread creates a paradox. On one hand, ETFs offer simple, lawful market access. On the other, they jar with the values that underpinned the blockchain industry: decentralisation, censorship-resistance and independence from third parties.

Рассылки ForkLog: держите руку на пульсе биткоин-индустрии!