Strategy holds bitcoin worth tens of billions of dollars and is increasingly tapping retail capital via securities issuance.

ForkLog examined how Michael Saylor’s company is structured, why critics call it a pyramid scheme while supporters see an example of effective risk management, and what’s behind the recent sale of part of its crypto reserve.

Where Strategy stands now

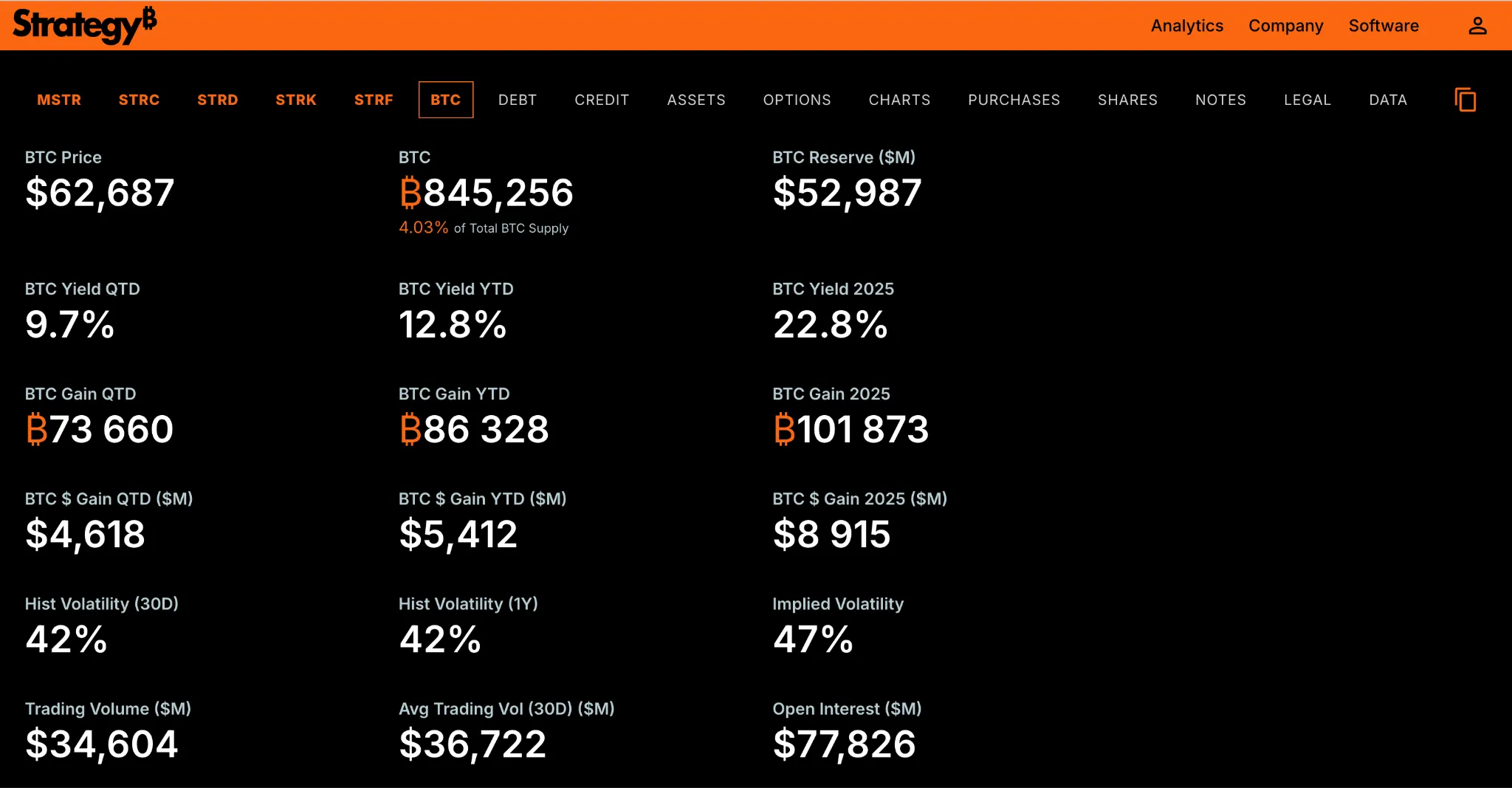

Strategy — the largest corporate holder of bitcoin — had more than 845,000 BTC on its balance sheet as of June 9, 2026. The blueprint is simple: raise capital in markets and buy the original cryptocurrency. The complexity lies in the instruments the firm uses and who sits on the other side of the trades.

In its latest move the company bought 24,869 BTC for roughly $2 billion and simultaneously retired $1.5 billion of debt. Key detail: 95% of the purchase funding came not from common-stock sales, but from placing STRC preferreds (Stretch). Common shares accounted for just 5%.

That shift has dominated debate in the crypto community.

How the company’s finance machine works

Strategy taps several funding channels.

Common stock (MSTR) — issued via an ATM program. Each new sale dilutes existing holders, making the ATM a frequent sore point for shareholders.

Convertible bonds — a tool for institutions. Investment banks sell exposure to MSTR through them. Some of these bonds carry a zero coupon but include the right to convert into stock at preset prices.

Preferreds, including STRC, are a different story. According to Blockspace Live hosts Charlie Spears and Colin Harper, they’re a “retail game”: institutions rarely buy them, and if they do, it’s a small sleeve. STRC pays roughly 11% in dividends.

The funding mix depends on market conditions. When bitcoin volatility is low and prices are rangebound, demand for new stock is thin — selling would mean “unfavorable pricing.” In those stretches STRC is cheaper to issue. The trade-off: preferreds require cash dividends, and those obligations persist.

The pyramid debate: the case for and against

Whether Strategy is a pyramid scheme has been debated for years. On Reddit, analyst Mark Meldrum’s breakdown sparked a long discussion. Proponents argue current investors are effectively paid from fresh issuance, while bitcoin on the balance sheet delivers only “theoretical” profits until it’s sold.

The counterpoint in the same thread: borrowing against assets to invest is standard practice. It’s routine in real estate and equities, and the principle alone doesn’t make a model a pyramid. The difference is that Strategy buys a volatile asset without a steady price.

Similar themes surface elsewhere — for example, in a LinkedIn post where private-capital manager Sasha Jovanovic reviews the topic through a corporate-finance lens.

He argues the company uses bitcoin as its numeraire. In 2025, the stock’s return measured in the original cryptocurrency was 22.8%. Jovanovic emphasized the figures are transparent and auditable, whereas Ponzi schemes hide or invent returns.

Strategy directs new capital toward buying digital gold for reserves, not paying earlier investors. That creates a “flywheel”: rising prices enable issuance of bonds and additional stock for further purchases.

Jovanovic added the company doesn’t hide volatility — it monetizes it. Over the year, the structure issued $7 billion of debt. He stressed that even with a 90% price drop (to $8,000), reserves would cover net debt.

He concluded that pyramid accusations reflect a misunderstanding of the company’s balance-sheet mechanics and its unconventional treasury management.

Users on the r/CryptoCurrency subreddit point out how Saylor’s own statements highlight MSTR’s vulnerabilities. Skeptics compared the setup to the 2008 mortgage crisis, when financial firms also used high leverage and overvalued assets. Others noted Strategy’s reserves are too small to cause a systemic shock to the broader economy.

In practice the risks look more modest. Convertible debt is small relative to bitcoin reserves, and many coupons are near zero. That reduces the odds of a forced unwind, though the question remains: how to meet obligations without selling bitcoin.

Why sell bitcoin

The headline in recent weeks was a small sale of the original cryptocurrency, even though Saylor has repeatedly said he wouldn’t sell digital gold.

Never sell your Bitcoin.

— Michael Saylor (@saylor) February 2, 2025

On the Blockspace Live podcast, the sale was framed more as a signal than a move for cash.

The message: Saylor is signaling he isn’t so rigid that reserves are never touched. A categorical refusal to sell would be more troubling. The amount is too small to move the balance sheet — but it’s still widely discussed.

Another concept surfaced — reverse reflexivity. Previously, the loop worked like this: Strategy issues stock, buys bitcoin, and MSTR climbs. Now the logic flips. When the company sells digital gold, its shares drop more than bitcoin itself, and the sale adds pressure to the asset’s price. Scale brings advantages but also creates a trap.

The public arena is shifting in parallel. Blockspace Live participants noted Saylor now faces visible “competition for attention” — for example, Jeff Walton, who projects a more accessible, risk-aware voice.

Coffeezilla just debated Jeff Walton for an hour about bitcoin and Michael Saylor’s digital credit business.

If you don’t know him, @Coffeebreak_YT has become the most popular YouTuber focused on exposing crypto scams and is skeptical of the strategy. pic.twitter.com/8LWYDxyY5a

— Documenting ₿itcoin 📄 (@DocumentingBTC) May 7, 2026

Why retire those specific bonds

Spears and Harper analyzed Strategy’s less obvious step: the company repaid convertible bonds due in 2029 with a conversion price above $670. Notably, that wasn’t the nearest maturity and didn’t carry the highest coupon.

The 2029 notes have minimal intrinsic value: the market ascribes almost nothing to the embedded conversion option, valuing it near zero. That means the firm spends the least cash per dollar of debt retired — making them the cheapest for early takeout.

This speaks less to a view on equity value than to a drive to cut debt with the lowest cash outlay per unit retired. After the deal, about $6.5 billion of convertible debt remains, with maturities through 2032.

Hence the internal tension in the model. MSTR holders care about less dilution. STRC holders want cash to flow freely to dividends. It’s hard to please both at once, and the pendulum now swings toward STRC.

Who actually holds the paper

Primitive Ventures managing partner Dovey Wan adds context: about 80% of STRC holders are retail investors, and roughly 40% of MSTR holders are retail as well. Wan also acknowledged that the “embedded Ponzi” thesis in STRC appears not to hold up.

80% of $STRC holders are retail investors

40% of $MSTR holders are retailWas thinking STRC was an insiti ponzi but apparently not 🤔

— Dovey “Rug the fiat” Wan (hiring) (@DoveyWan) May 8, 2026

That explains why the dividend question is so sensitive. By Blockspace Live’s estimate, the balance sheet covers roughly six months of STRC payouts. After that the company effectively has two options: reduce the STRC dividend or sell bitcoin.

It’s the second path that worries the market. The issue isn’t the tiny amount sold, but the fear sales could grow to cover dividends. The Blockspace Live hosts see the probability of a “blowup” as low, but with $50 billion in bitcoin even a hint of large-scale selling makes participants nervous.

At the same time, the podcast linked the recent crypto downturn less to Strategy and more to capital rotating into artificial intelligence — amid expected IPO SpaceX, Anthropic and OpenAI. Bitcoin volatility is near its lowest in almost ten months.

What critics say

Euro Pacific Capital President Peter Schiff said MSTR is “the biggest Bitcoin buyer and the biggest Bitcoin loser.”

$MSTR Is the biggest Bitcoin buyer and the biggest Bitcoin loser. Strategy has been buying Bitcoin for over five years, and so far that “investment” has netted an unrealized $12 billion loss. If a genius like @saylor can’t even make money in Bitcoin why should anyone else try?

— Peter Schiff (@PeterSchiff) June 4, 2026

By his estimate, after more than five years of buying, the unrealized loss has reached $12 billion — and “if a genius like Saylor can’t even make money in Bitcoin, why should anyone else try?”

Institutional voices have joined in. Arca Chief Investment Officer Jeff Dorman called Strategy’s preferreds “out of control,” pointing to roughly $15 billion of such issuance.

Attention is also rising in major media. The New York Times published a substantial feature on Saylor and Strategy — a sign the story now extends well beyond crypto.

What to watch next

Strategy isn’t a classic pyramid in the legal sense. In practice, everything hinges on two things: bitcoin’s price and the ability to attract new capital.

The near-term questions boil down to three:

- Whether the company can keep servicing STRC dividends without sizable bitcoin sales.

- Whether it can retire the remaining $6.5 billion of convertible debt without large asset disposals.

- Whether retail demand for preferreds holds if bitcoin jumps and makes common stock a more convenient funding tool.

For now, Strategy is walking a line between market signaling and hard obligations.